BSP Gov. Felipe Medalla Message

BSP Gov. Felipe Medalla Message Read More »

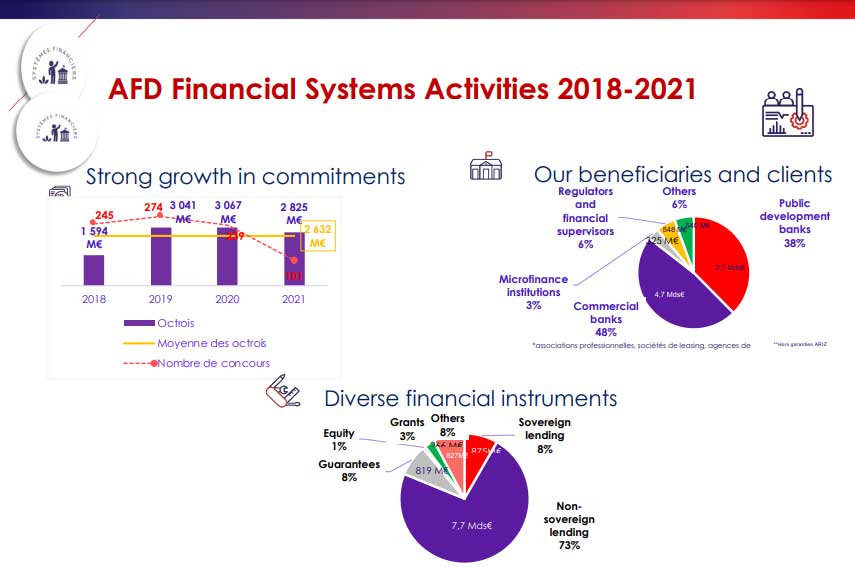

Corporate Governance Rural Banks’ Resilience and Relevance: Rising Above the Challenges PDIC and Rural Banks: Rising Above the Challenges DA-ACPC&RBAP Opportunities and Cooperation Roadmap to Data Privacy Resilience Insights From The Pandemic Our Instapay Journey BSP Innovation and Technology Update Landbank Presentation Outline AFD Technical Assistance on capacity building to rural banks via RBAP under

69th Annual Convention & GMM Speakers’ Presentations Read More »

LIST OF CERTIFICATE OF CANDIDACY AND SECRETARY’S CERTIFICATE RECEIVED AS OF MAY 18, 2022 REGION NAME POSITION INDICATED IN THEIR COC RURAL BANK LOCATION FEDERATION / CONFEDERATION DATE RECEIVED MEMBERSHIP STATUS CERTIFICATE OF CANDIDACY SECRETARY’S CERTIFICATE NCR Leonard R. De Ocampo Director Bangko ng Kabuhayan (A Rural Bank) Inc. Pasig, Metro Manila Federation of Metro

LIST OF CERTIFICATE OF CANDIDACY AND SECRETARY’S CERTIFICATE RECEIVED AS OF MAY 18, 2022 Read More »

RBAP is hereby suspending the advertised Request for Expression of Interest (REoI) for an Implementing Agency to an AFD Technical Assistance announced on April 6, 2022 in order to UPDATE the version of the REOI and EXTEND the deadline of the submission. Please watch out for the announcement of the updated REOI details.